Market Recap, Week 3 Oct-7 Oct 2022 [ENG]

Market Recap, Week 3 Oct-7 Oct 2022 [ENG]

This is a very complicated and unique year in many ways.

Let us summarize them below:

The world is emerging from a global pandemic.

We are witnessing a war between the US and Russia, and wars as they are inherently inflationary.

This is an election year in the United States, with voters heading to the polls in less than six weeks.

In the past 40-50 years, we have not seen such a sell-off of bonds and stocks at the same time. We are witnessing a once-in-a-lifetime event, in the way we are witnessing the destruction of wealth across all asset classes.

If 2022 were closed today, a classic 60/40 balanced portfolio would have reported losses of -22%, only in 1931 did worse with -27%.

Let's now turn to the situation in the SP500 weekly.

No change since last week's analysis, which you find in the Market Recap, Week 26 Sept-30 Sept 2022, except that we have drawn a potential reversal candle that will be confirmed IF and ONLY IF we exceed the area 3800 points and not Before. We are entering the earnings season and this, along with what we will see later, can give us a direction for prices.

All other considerations made on Sentiment and breadth continue to apply Market Recap, Week 26 Sept-30 Sept 2022 and Daily Report, October 05th, 2022

Short-term scenario – Sp500 chart

In the Daily Report, October 05th, 2022, we said that although the first three days of the week had been very positive, we should have curbed the bullish enthusiasm at least until the bearish channel broke.

The conclusion, for now, is that we must respect this trend.

The next key economic report will be next Thursday when we have the consumer price index (CPI) reading coming a day after the FOMC minutes, both of which could be revealing for price.

Then we would have the release of the earnings reports of the main American banks.

So it is possible that we will still see weakness unless some kind of positive surprise gives the bulls something to work on. Will it come from the earnings? Here is an image that summarizes the main earnings of the week.

#TSM, Delta Air Lines #DAL, Morgan Stanley #MS, Citigroup #C, Blackrock #BLK, Wells Fargo #WFC, and Domino's Pizza #DPZ.")

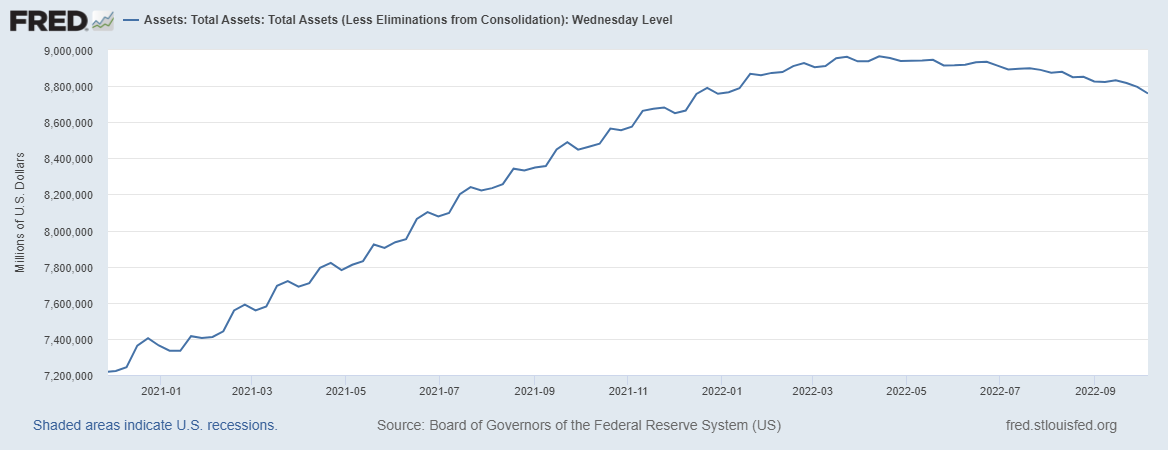

The Fed is (finally) starting to accelerate the Quantitative Tightening

The Fed's balance sheet has dropped to about $8.8 trillion in recent months

The image above shows the trend of the Fed's balance sheet in recent months; a downward trend that coincided for the most part with a downward trend in the share price.

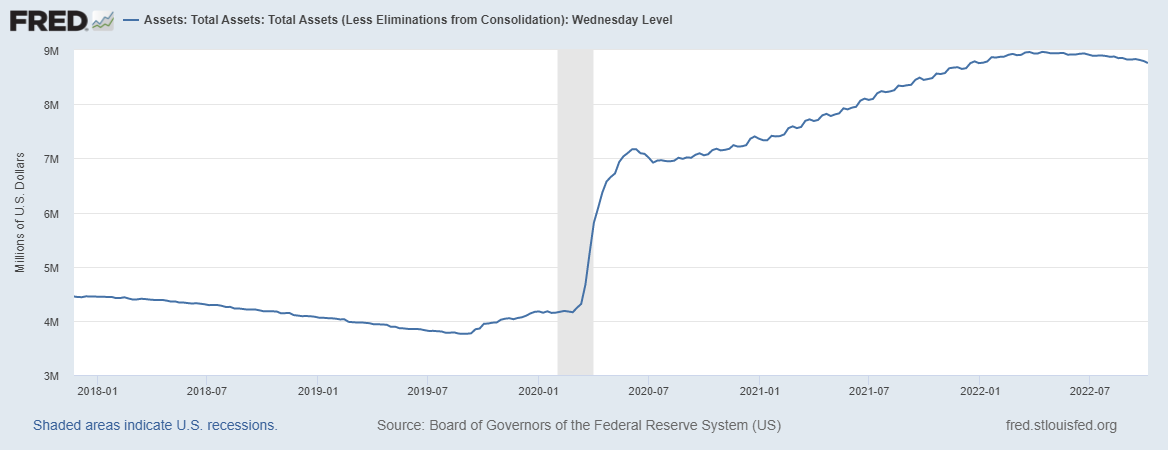

Enlarging the graph, considering all the assets that the US Fed has we realize the extent of this “bubble” (note the surge in the COVID-19 period, when the Fed was extremely accommodating to support the entire economy)

While equities have fallen significantly from their highs, some as much as 80-90% from their peaks, the Fed's assets have barely moved from the general pattern.

It is rather ridiculous that a mere $95 billion a month reduction in the balance sheet of the world's most influential central bank took so much sprint from the equity markets to -25% from all-time highs and the total sell-off of bonds.

Imagine the horror if the Fed returns to pre-pandemic levels at around four trillion dollars!

It would be a real Armageddon of all financial assets and more!

It is a catastrophic hypothesis, and we do not believe that this will happen, as there is and will be structural support for the entire economy, but there is still a minimal probability.

In the Daily Report, September 13th 2022 you find a hypothetical scenario for 2023 macro if interest rates remain high for an extended period

The macro scenario we are going through reminds us of a quote from Sir. Winston Churchill.

"If you're going through hell, just keep going"

How we use the bond market

In recent weeks, we have been keeping our eyes on the bond market waiting for signs of a restart, this is because we believe that this market will also be a fundamental proxy for the stock market.

There are days in the bond market when volatility stands at 4-5% as if they were stock memes, and it is difficult to find something similar in recent history other than a few isolated cases like the pandemic crisis, but there was indeed a pandemic.

As we see the action on the TLT (20-year bonds):

The TLT should find some support around 99-100, NOT because all the problems in the world are solved today or tomorrow, but only because a TLT below area 100 could become a failure symbol.

This is why we think the Fed will “panic” and put a limit on falling bonds.

We, therefore, think that the TLT is close to a significant low, and when we say significant we mean a training process that could last 2-3 months or even longer.

If things fail, and if we continue to sell bonds, we think we will have a few more volatile months ahead in the equity markets.

So while the Fed may not be interested in saving equities, it could be busy saving bonds.

So, yes, we think that bonds will have to be supported from here at some point forward and when that happens, even riskier assets like equities will benefit.

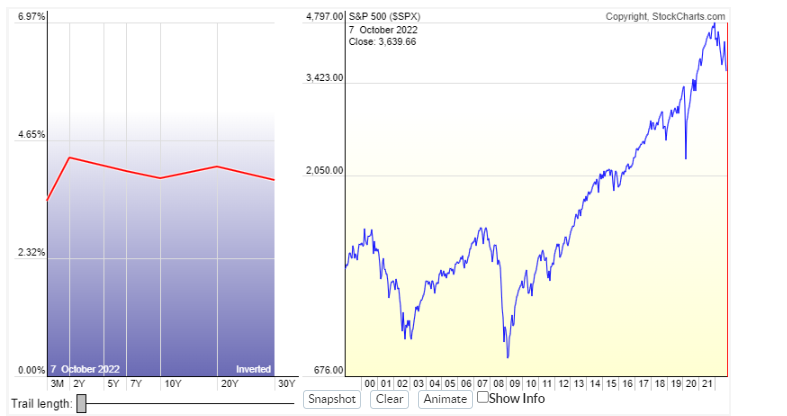

Special chart—A yield curve

As an additional indication that this is an anomalous year, let's look at the yield curve. A few weeks have taken this shape which has been a harbinger of the biggest recessions and bear markets in recent decades, i.e., an inverted shape.

An inverted curve has never been a problem for the stock market, at least initially.

From the data available, it is the first time that the curve has taken such a shape after a -25% from the all-time highs of the stock market, adding further pressure to the economic and financial system of the United States.

However, there is a small glimmer of hope, if we consider only the first part of the curve, the difference between three-year and 10-year yields (10Y-3M). This is the most impacted by the FED interest rates in the short term.

While the situation on maturities from 2 to 10 years is a reversed shape (which is not a good thing), we observe that the maximum drawdown of the stock markets is reached 12 months after the inversion of 10Y-3M

Currently, we are not yet in a land of COMPLETE inversion and this bodes well but, as we have seen, this is a unique year as stated initially. Therefore, we need extreme caution, a critical eye, and patience.